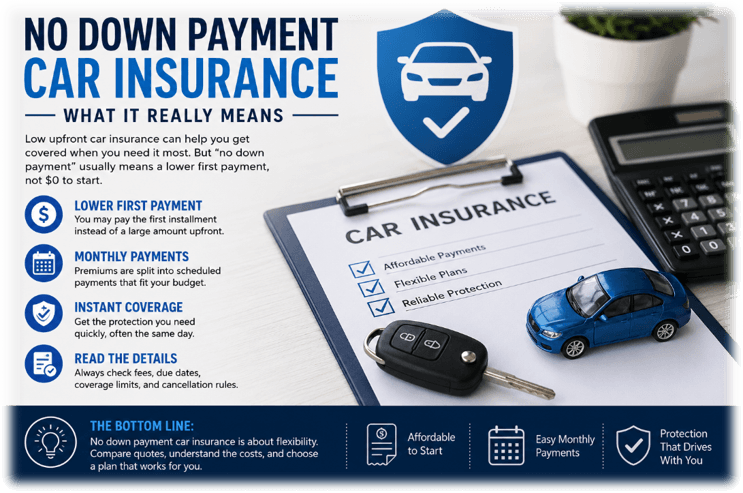

What Drivers Should Know Before Choosing a Low Upfront Car Insurance Plan

For many drivers, the hardest part of buying car insurance is not always the monthly premium. It is the amount required to start the policy. When someone has just bought a car, moved to a new state, changed jobs, or had a recent policy lapse, even a normal first payment can feel difficult to manage.

That is why low upfront car insurance options have become popular among drivers searching for flexible ways to get covered quickly. These plans are often described online using terms like “no down payment,” “no deposit,” or “low down payment.” However, drivers should understand what those phrases actually mean before choosing a policy.

In most cases, a low upfront plan does not mean the insurance company starts coverage for free. It usually means the driver may be able to begin coverage by paying only the first scheduled instalment instead of a larger portion of the full premium. For a clearer explanation of how this wording works, this guide on no down payment car insurance explains why the phrase usually refers to a lower starting cost rather than a true zero-dollar policy.

Why the First Payment Matters

Car insurance is a legal contract. Once the policy becomes active, the insurer is taking on risk. If a covered accident happens after the effective date, the company may be responsible for handling claims according to the policy terms. Because of that, insurers usually require some payment before coverage begins.

Depending on the company, the first payment can have another different name. Some insurance companies refer to it as the first payment. It can also be referred to as a down payment, deposit, first premium or amount due today. The label is not as significant as the details that support it.

Before choosing a policy, drivers should review the main payment details carefully:

| Question | Why It Matters |

| How much is due today? | This tells you the real cost to start the policy. |

| When does coverage begin? | You need to know the exact effective date and time. |

| What is the monthly payment? | A low first payment may lead to higher monthly iinstalments |

| Are there instalment fees? | Monthly billing can sometimes increase the total cost. |

| What happens if a payment is late? | Missed payments can lead to cancellation or a lapse in coverage. |

The easiest to start a policy is not necessarily the lowest cost policy overall. The most suitable always is the one that can be balanced with both the initial payment that is affordable as well as a month to month cost that is within the driver’s budget.

“No Down Payment” vs. “Low Down Payment”

When you see the term “no down payment,” they may be implying that this is not something that’s due before you start coverage. Unfortunately, most reputable auto insurance companies still need an initial payment. Typically, that charge is part of the premium and not an additional payment that goes away.

A better way to understand the terminology is this:

- No down payment: usually means no large extra deposit beyond the first payment.

- Low down payment: means the first payment may be smaller than paying a larger portion upfront.

- Monthly car insurance: means the premium is divided into scheduled instalments.

- Same-day coverage: means the policy may start quickly after the application and payment are completed.

Not every policy is created to have zero dues today for budget-conscious drivers. The idea is to discover a policy that has a reasonable amount of money that is due now and one in which the payments don’t cause another issue next month.

What Can Affect the Amount Due Today?

The cost to begin a car insurance coverage policy can be quite different. There are multiple risk and pricing factors that insurance companies consider for two drivers in the same city who are seeking quotes.

Common factors include:

- Driving history: accidents, tickets, and serious violations can increase the premium.

- Vehicle type: newer, more expensive, or high-risk vehicles can cost more to insure.

- ZIP code: Insurers may consider claim frequency, theft risk, traffic density, and repair costs in the area.

- Coverage level: Liability-only coverage usually costs less than full coverage with collision and comprehensive.

- Prior insurance: a recent lapse may make coverage more expensive.

- Payment plan: paying monthly can reduce the starting cost, but may includeinstalmentt fees.

That’s why it’s essential to shop around for quotes. One company might ask for a bigger initial fee and another may allow flexibility in billing for the same driver.

When a Low Upfront Plan Can Make Sense

Some typical scenarios where a low initial payment might be beneficial. For instance, a driver can require coverage in the same moment that the car is registered, meets the requirements of the lender, to prevent the lapse of coverage, or to legally travel after purchasing a car.

It can also be helpful for the drivers who are making an attempt to manage cash flow. In some situations, it may be less expensive to pay the total six month premium all at once but not everyone can afford this. While the monthly expenses may be a bit more, monthly billing can make coverage more convenient to begin.

| Situation | Why It Helps |

| You just bought a car | You may need proof of insurance quickly. |

| You are switching insurers | A lower first payment can make the transition easier. |

| You recently had a lapse | Getting covered again quickly may help avoid more problems. |

| Your budget is tight | Monthly billing may be more manageable than paying a large amount upfront. |

The main thing is, don’t select a policy simply because of the initial payment. Before choosing a policy, drivers need to compare overall policy pricing, coverage, deductibles, fees, and policy cancellation.

How to Compare Low Upfront Car Insurance Quotes

Always compare quotes with the same coverages. Different quotes may not be easily comparable, as one may be a state-minimum liability quote and another may have collision, comprehensive, roadside assistance, and rental reimbursement coverage.

A smarter comparison should include:

- Same liability limits: Compare equal coverage limits whenever possible.

- Same deductibles: Higher deductibles can lower premiums but increase out-of-pocket costs after a claim.

- Same vehicle information: Make sure the VIN, mileage, and usage are accurate.

- Same driver details: Include all required household drivers to avoid quote changes later.

- Total policy cost: Look beyond the first payment and review the full-term cost.

Additionally, you need to consider if the quoted price is inclusive of all fees. Some plans might seem more affordable upfront, but be less appealing when monthly billings or policy fees are taken into account.

Warning Signs to Avoid

Not all the offers that start at a lower rate are great. Promotions that are too general or too good to be true should be approached with caution by the driver.

Watch out for:

- Claims that coverage begins without any payout up front.

- There is no specific name for the insurance company or agency information.

- Significant price changes at the time of purchase

- There is no clear effective date or proof of insurance.

- The option of buying without really reading the policy.

- Missing information on fees, cancellation or renewal conditions.

A legitimate insurance offer ought to be clear about the amount required today, the term of the policy, the coverage limits, deductibles, charges, and when the quantity will be paid. If they do not have those details, then it would be wise to come up with a few questions before sending any money!

Final Thoughts

If you are an individual who requires help with car insurance and you just do not have the available cash to pay for it completely, it may be helpful for you to find low-upfront car insurance. But the term “no down payment” is not to be taken at face value. In most situations, it does not mean that you will not have to pay anything out of pocke,t and idoesll not mean that you are covered for free.

A better way to go is to look at actual quotes, see how much is paid today, check the monthly schedule and be sure the policy offers the coverage you need. A good plan should be affordable to begin, practical to maintain, and make sense in that you know precisely what you are purchasing.

Popular on OTW Right Now!

About The Author

Gagan Bhangu

Founder of otechworld.com and managing editor. He is a tech geek, web-developer, and blogger. He holds a master's degree in computer applications and making money online since 2015.