Sms lån in norway: What it is, what it costs, and what you need to now before you apply

The term sms lån gets searched thousands of times every month in Norway and most people searching for it want the same thing: a small amount of money, fast, without too much hassle. The idea behind it is simple enough, borrow money by sending a text message and get the funds in your account within hours. But the reality of how sms lån works today, what it actually costs, and who can qualify is quite different from what many people expect.

A country that was ready for this kind of borrowing

Norway was among the pioneer nations in the world to take the cashless economy seriously. By the end of the 1990s, mobile phones had already become mainstream in Scandinavia, and Norwegian banks were not slow in capitalizing on this. Customers were able to check balances, remit funds, and settle bills right out of their phones, way ahead of what Europeans would follow.

The concept went viral in Norway, Denmark, and Sweden. To some extent, it was a real new approach towards short-term financial troubles. And to a lot of people, it was handy– until the expenses began to accrue to the mortgagers who had not really comprehended what they had entered into.

How the sms lån actually worked — And why people used it

The process was very simple in the beginning. A borrower would have an agreement with a lender beforehand, and he or she would be given a personal PIN code, after which he or she would send a text message to the lender requesting his or her amount. The lender would handle it and transfer the money straight into the bank account of the borrower in most cases within a few hours. There was no credit check, no income verification, and no paperwork of any kind. For a resource that explains what these loans looked like and how today’s fast digital loans compare, forbrukslån.no/sms-lån gives a clear and up-to-date overview.

Here is what made the original model different from a regular bank loan:

- No branch visit needed; the whole thing happened over a text message.

- No paper forms, payslips, or income documents were required.

- Money landed in the borrower’s account the same day, often within hours.

- Loan amounts were small, usually between NOK 1,000 and NOK 15,000.

Why Ordinary People Were Drawn to It

The appeal was not difficult to follow. An unexpected bill, a car breakdown, a few days to payday, and an sms lan required virtually nothing when a person was in need of money. There are no approval waiting days, no sitting face to face with a bank manager, and no reason as to why you require the money. This was a viable alternative to people who had a thin or defective credit history who would otherwise have been rejected by a conventional bank. The entire product was speed and simplicity.

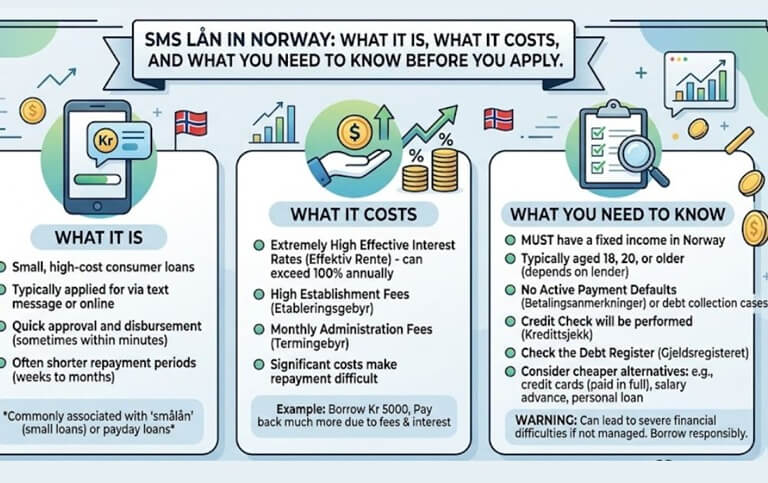

What an sms lån actually costs — The numbers you need to know

This is the one that most individuals are surprised about. Due to the unsecured nature of the sms lan and fast mobile loans, that is, there is no security of any form attached to it, the lenders will provide the loans at a higher rate to offset the risk. The expenses might mount very fast when you are not attentive.

Here is a realistic breakdown of what you can expect to pay:

- Establishment fee: Typically around NOK 900, though some lenders charge based on the loan amount.

- Monthly installment fee: Usually between NOK 40 and NOK 200 per month.

- Effective interest rate on NOK 20,000: Can range from 20% to 30% annually.

- Effective interest rate on NOK 50,000: Usually lower, around 15% to 20%.

- Repayment period: Most fast loans must be paid back within 12 months.

When the authorities decided enough was enough

Norway is the first Scandinavian nation to take action as the debts soared, and they started to complain. As early as 2006, senior governmental elements went on record to denounce the industry. New regulations came into place, according to which credit checks were mandatory prior to any loan issuance. That single modification shattered the initially existing sms lån model. Once one was required to conduct a legitimate credit check, the entire send a text and have money in minutes deal was ruined.

The New Rules That Changed Everything

The new lending regulation of Norway, which has gone through many changes and is divided into consumer loans, car loans, and credit lines, has the following requirements that the lenders must comply with before giving any loan:

- Verify the complete income and current debt of the borrower.

- Ensure that the borrower would be able to meet his costs in case interest rates increase by 3 percentage points.

- Maintain total debt to a permitted level of debt-to-income ratios.

- Check with BankID to ensure that the borrower is who he claims to be before signing any agreement.

- Norway vs. Denmark vs. Sweden SMS loan regulations in a nutshell.

Norway vs. Denmark vs. Sweden — SMS loan rules at a glance

| Rule | Norway | Denmark | Sweden |

| Credit check required | Yes (since 2006) | Yes (all amounts) | Yes (introduced later) |

| APR cap | No formal cap | Yes | No formal cap |

| 48-hour payout hold | No | Yes (high-APR loans) | No |

| BankID / digital ID required | Yes | Yes (NemID) | Yes |

| Predatory lending ban | Partial | Full | Partial |

| Classic sms lån still available | No | No | No |

What to check before you apply for a fast loan today

The traditional sms lån does not exist in its original version in Norway anymore. The digital consumer loan that you have got today, when you search one, is a fast digital consumer loan – applied with your smartphone, processed immediately, and deposited in your bank. The procedures are not new, and they now have good checks in the background. The following are the things worth checking before you apply to any of these products:

- Your credit score

- Eligibility basics

- The effective interest rate

- Total repayment amount

- Whether you actually need it

Conclusion

A good example of what can occur when an idea that has a sound purpose gets ahead of the regulations that are set to safeguard people is the sms lan story. The very idea of borrowing a small sum in a short time using your phone was not the issue. The issue was that there were no checks, no boundaries, and no actual means of borrowers to know what they were entering into. Norway was the first to do that, Denmark the farthest, and Sweden had learnt by being too late. What remains today is a more cautious adaptation of the same concept, quick, phone-based lending within the framework of appropriate consumer protection laws. Even a speedy digital loan can be a useful short-term resource, assuming that you know the costs involved in borrowing and only take them in a comfortable amount that you can repay.

Popular on OTW Right Now!

About The Author

Gagan Bhangu

Founder of otechworld.com and managing editor. He is a tech geek, web-developer, and blogger. He holds a master's degree in computer applications and making money online since 2015.