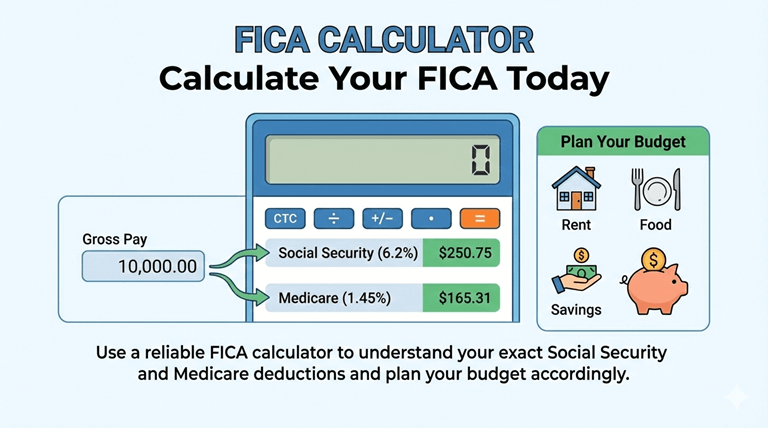

FICA Calculator: Social Security and Medicare Taxes

FICA (Federal Insurance Contributions Act) taxes fund Social Security and Medicare through mandatory payroll deductions of 7.65% for most workers—6.2% for Social Security and 1.45% for Medicare. In 2026, Social Security tax only applies to the first $168,600 of earnings, while Medicare tax applies to all wages, with high earners paying an additional 0.9% on income over $200,000. Self-employed individuals pay both the employee and employer portions (15.3% total) but can deduct half as a business expense.

Understanding FICA Tax Components

There are actually two separate parts of the tax that your FICA calculator works with that occur in two separate line entries in your pay stub. The Social Security tax, formally referred to as Old-Age, Survivors, and Disability Insurance (OASDI), has a limit on the maximum income that annually varies with inflation.

The Social Security wage base rose to 2026 and amounts to $168,600, and this implies that once you earn above this wage base in the calendar year, you no longer pay Social Security tax. Nonetheless, there is no limit on income subject to collection by Medicare tax, and top earners are subject to an extra 0.9% Medicare surcharge on wages above certain levels.

The major FICA tax specifications of the year 2026 are:

- Social security rate:2% on wages up to the amount of $168,600 a year.

- Maximum Social Security Tax: High earners—$10,453.20 per year.

- Medicare Rate:45% of all wages, without any income limit.

- Extra Medicare Tax: It is 0.9% applied to income exceeding $200,000 (single taxpayer) and $250,000 (married filing jointly taxpayer).

- Employer and Employee FICA:3% each

- FICA Exemptions: Some students and government workers are in alternative pensions.

According to the Congressional Budget Office, FICA taxes provided the government with more than $1.51 trillion in federal revenue in 2025, which is about 34% of the total federal revenue that would have been collected by the fiscal year.

FICA Impact Across Income Levels

The FICA calculator tool shows how these compulsory deductions impact differently according to their income. Lower-income employees remit FICA on their full wages, and high-income employees eventually cease to pay taxes to Social Security in mid-year after reaching the wage base threshold.

| Annual Salary | Social Security Tax | Medicare Tax | Additional Medicare | Total FICA | % of Gross |

| $40,000 | $2,480 | $580 | $0 | $3,060 | 7.65% |

| $80,000 | $4,960 | $1,160 | $0 | $6,120 | 7.65% |

| $168,600 | $10,453 | $2,445 | $0 | $12,898 | 7.65% |

| $250,000 | $10,453 | $3,625 | $450 | $14,528 | 5.81% |

| $500,000 | $10,453 | $7,250 | $2,700 | $20,403 | 4.08% |

Source: Social Security Administration 2026 Contribution and Benefit Base

This analogy illustrates that employees whose incomes are $168,600 and below pay the entire rate, which is 7.65% FICA, whereas those who earn $500,000 pay an overall rate of 4.08% because of the social security wage ceiling, cutting the effective rate of FICA to 4.08%.

Real-World FICA Calculations

Case Study 1: Registered Nurse in Arizona

Working at a hospital in Phoenix, Emily has an annual income of $78000. Her FICA calculator illustrates the deductions in social security of $186 biweekly (6.2% of $3,000) and in Medicare of $43.50 (1.45% of $3,000). The FICA contributions to Emily will amount to a total of $5,967 as an annual contribution, which will reduce her gross net salary by $229.50 every two weeks before other deductions are made, such as the federal income tax, health insurance, and retirement contributions.

Case Study 2: New York Investment Banker

David works as an investment banker in Manhattan, earning a sum of $350,000. This calculation in FICA is very different from Emily’s because it has income requirements to calculate his income. David has attained his Social Security wage base of $168,600 by the beginning of August, after which his biweekly paychecks have escalated by $417 when Social Security withholding ceases until the end of the year. Nonetheless, his Medicare tax remains 1.45%, together with an extra 0.9% surtax on income above $200,000 at 2.35% of his highest income brackets.

The examples demonstrate how the gross-to-net salary US calculation needs the comprehension of the progressive nature of FICA, in which high earners get to enjoy a wave of mid-year salary increments once they hit the Social Security wage base threshold limit.

Self-Employment and Employer Matching

Employers are matched by the employer FICA, in which the companies pay the same amount as you towards your Social Security and Medicare tax. This implies that your employer will contribute an extra 7.65% to your contributions, which would double the FICA funds in your future benefits.

Paycalculator.ai will automatically compute both the employee and the employer FICA amounts, which will make you realize how much the real cost of employment taxes is. This is a complete calculator where you can see your entire tax obligation, including federal income tax, state tax, and all FICA rates at present rates in the year 2026.

The working self-employed bear more FICA obligations since they pay the employee and employer sides, amounting to 15.3% of the net self-employment income. The IRS tax law, however, permits the self-employed workers to assume the employer-equivalent portion (7.65%) on the calculation of adjusted gross income, but to deduct the extra tax load in part.

Tax policy expert Dr. Sarah Williams of the Tax Policy Center says that the calculations based on FICA are an important part of financial planning since mandatory taxes make a huge difference to the amount that workers take home at the end of the day, although, she says, many workers do not notice that they are contributing valuable Social Security credits and Medicare eligibility with each paycheck contribution.

FICA Exemptions and Special Cases

Some employees are also exempt from the FICA tax under given conditions that are specified in the Internal Revenue Code. Full-time working students at their university may receive an exemption on campus wages on FICA, and certain employees in state and local governments have their contributions to other types of pensions.

Conscientious objections can be sought by religious groups, and temporary exemption is given to nonresident aliens in some visa categories in their first year of residence in the United States. Such exemptions must be documented and approved by the IRS to prevent errors in withholding and subsequent punishments.

FICA vs. Your Total Tax Withholding

When you use a tax withholding calculator, you are usually trying to solve one mystery: “Where did my gross pay go?” It is important to understand that your total withholding is actually split into two main categories:

- Federal Income Tax: This varies based on your W-4 settings and filing status.

- FICA Taxes: These are mandatory payroll taxes for Social Security and Medicare.

Even if you have zero federal income tax withheld, you will almost always still see FICA deductions on your paycheck. Use the calculator above to see exactly how much of that “gap” is going toward your future benefits.

Best Tool for FICA Tax Planning

Proper use of the FICA calculator will change how you view the amount deducted from your paycheck and also allow you to handle your financial plans more efficiently in the course of your career life. Paycalculator.ai is a real-time FICA calculator considering wage base limits of 2026, the Medicare surtax limit, and a full gross-to-net analysis of US salaries.

Critical FICA planning knowledge:

- The high earners can have their mid-year increases in their paycheck when the Social Security withholding ceases once they have reached the wage base.

- The self-employed workers are required to pay the entire FICA rates but are allowed half the deductions, as they are expected to pay the extra tax amount.

- With employer matching, your FICA amounts are doubled, and you accumulate considerable Social Security and Medicare benefits throughout your working life.

Calculate your FICA today: Use a reliable FICA calculator to understand your exact Social Security and Medicare deductions and plan your budget accordingly.

Frequently Asked Questions

Q1: What does FICA stand for, and what does it fund?

FICA is an initial of the Federal Insurance Contributions Act. It finances social security retirement, disability, and survivor benefits, and Medicare healthcare benefits, which cover the aging Americans who are 65 years and above, based on mandatory payroll taxes.

Q2: Can I opt out of paying FICA taxes?

No, the majority of employees will not be able to choose not to pay FICA taxes. FICA exemption is only applicable to certain exemptions, such as an exception for certain students, members of religious organizations with established exemptions, and a few workers under government-defined pension schemes.

Q3: Why does my paycheck increase mid-year as a high earner?

You will earn more as you get to the Social Security wage base of $168,600 in 2026. Then, at this point, Social Security withholding ceases, and you get an increment of 6.2% of the rest of the year as an addition to your take-home pay.

Q4: Do FICA taxes provide any personal benefits?

Yes, FICA taxes are credits you have achieved in building the Social Security that you will use in retirement, and set up your Medicare. Increased earnings and contributions to FICI in a lifetime translate to higher Social Security retirement benefits.

Q5: How do FICA taxes work for self-employed individuals?

Self-employed workers will pay a total of 15.3% of FICA (employee and employer parts) on net self-employment income. But the extra burden may be borne, at least in part, by the deduction by them of half (7.65%) of the adjusted gross income in determining the adjusted gross income.

Popular on OTW Right Now!

About The Author

Gagan Bhangu

Founder of otechworld.com and managing editor. He is a tech geek, web-developer, and blogger. He holds a master's degree in computer applications and making money online since 2015.